FAIT accompli?

Flexible average inflation targeting could mean that the Fed has a lot more work to do before they relent on rates.

A brief history of inflation in the US

The United States has existed in several different inflation regimes since its founding as excellently summarized in “A Short History of Prices, Inflation since the Founding of the U.S.” by Fernando M. Martin of the Federal Reserve Bank of St. Louis. The delineations of the regimes correspond approximately to the Civil War, creation of the Federal Reserve in 1913, the World Wars and concomitant Great Depression, and the Nixon Shock in 1971.

It's often claimed that war is inflationary but this is only half true. War is not directly inflationary. War is extremely expensive. The monetary policy actions countries employ to fund the war are inflationary. Martin succinctly lays out how every war in US history corresponds with an inflation event. It’s interesting that he doesn't directly mention the Vietnam war which corresponds to the nation's most severe inflationary episode to date but it is clear that the inflation of that period is what lead to the "run on the US dollar" that caused Nixon to "temporarily" suspend the dollar's convertibility to gold. Nevertheless, Martin and I agree that "the leading cause of high inflation is the willingness of central banks to finance government deficits by printing money.” He goes on to say:

Before World War II, episodes of high inflation were followed by periods of deflation, which explains the fact that the price level moved around a stable average. These inflationary episodes correspond to periods during which convertibility of the dollar to gold and/or silver was suspended to meet the demand for additional government revenue, most notably during the Civil War and World War I. Deflationary periods followed as convertibility was reinstated and prices returned to their pre-war levels. Although the price level was stable over the long run, inflation was very volatile during this period.

Peacetime deflation effectively paid back the devaluation of the currency caused by wartime inflation and restored soundness to the money. But since the creation of the Fed and in particular, since the abandonment of gold convertibility in 1971, the bias has been consistently inflationary with extremely rare dips into deflation. In other words, we've been on a wartime footing from a monetary policy perspective and that monetary debasement has never been paid back. Martin cites the lower volatility and removal of the deflationary swings as a win for the predictability of the economy. Let’s quantify the tradeoff. Using Martin’s numbers, before the Fed was created, average inflation was 0.4% and since then it’s been 3.5%. If we had persisted with an average 0.4% inflation since the Fed’s founding in 1913, a dollar would be worth $0.36. Not great, but not bad. At 3.5%, that same dollar is worth $0.02. He seems to accidentally make the argument that a dollar would be worth twenty times more if we had not established the Federal Reserve so I wholeheartedly disagree when he says:

Although average annual inflation since 1941 is higher, it is not dramatically higher than in the pre-Fed period: 0.4 percent vs. 3.5 percent. In contrast, volatility decreased tremendously: 13.2 vs. 0.8. Arguably, then, the costs were small while the gains large.

There is a huge difference between 0.4% and 3.5% inflation over economic timescales. If the tradeoff is between a nickel and a dollar, bring on the volatility.

The FAIT of fiat

In August 2020, after conducting their first ever monetary policy review, the Federal Reserve announced that it would adopt a policy of "flexible average inflation targeting," FAIT, in response to more than a decade of persistently low inflation since the Great Financial Crisis of 2008/09.

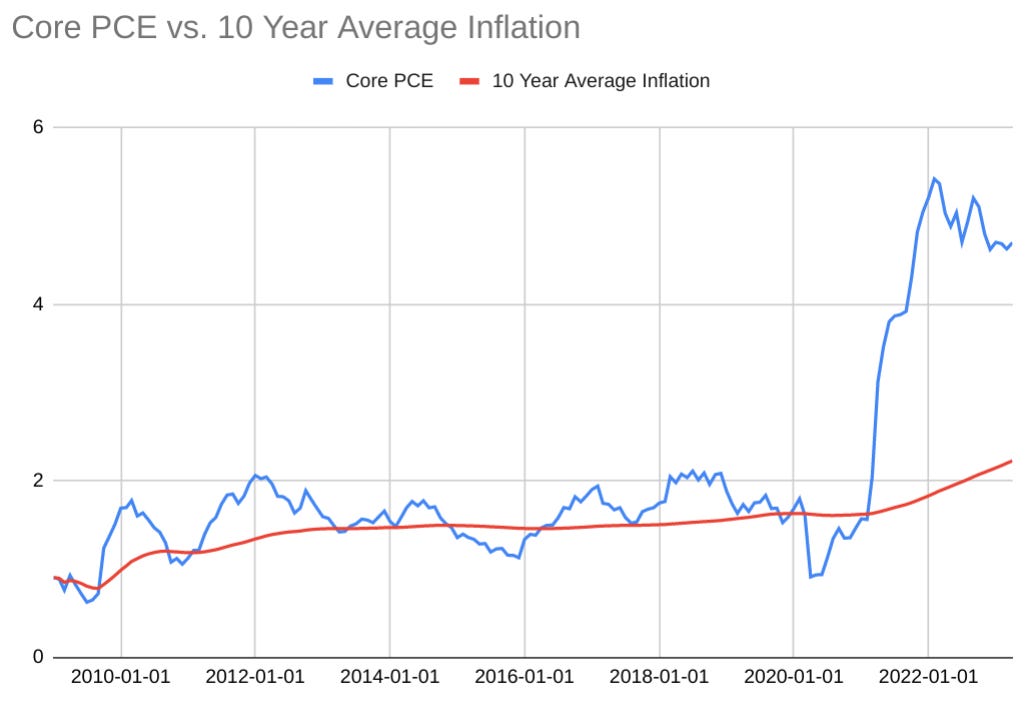

The principle behind FAIT is that the Fed would allow inflation to run above their 2% target until the average inflation level rose to that target. They give themselves significant latitude by stopping short of saying they would adhere to mathematical rigor in this regard but a recent look at inflation since the GFC alongside the average inflation yields an eye opening result.

For the first time since 2009, the average inflation since the GFC has reached 2%. Many have speculated that the Fed would pause after their next meeting but if they are true to their goal of controlling long run average inflation, there could be an argument that they need to continue their strenuous monetary tightness in order to prevent the average from trundling above their long run 2% average goal.

In Martin's analysis, he uses a 10 year average. If we apply a 10 year moving average instead of the 14 year average since the GFC to our previous chart, we've already exceeded a 2% average by a decent margin. A 10 year average is arbitrary but it is also probably reasonable given that business and credit cycles are probably on the order of this amount of time.

What's interesting to me is that the Fed and the rest of the world's central banks have kept interest rates low since the GFC until very recently and yet inflation remained persistently under their goal. It took a global pandemic, permanent supply chain disruptions, and in particular, a war before we got substantial inflation. Since inflation didn't result from easy monetary policy, why do policymakers believe that tight monetary policy will have the opposite effect? Nevertheless, they remain steadfast in their policy stance that higher interest rates are the medicine that is needed to bring inflation down so they are likely to stay the course.

A recently trendy metric that tries to read through the official headline inflation numbers is Truflation. It’s down to 2.85% and portends toward a continuing disinflationary trend. CPI and PCE react with a significant lag so Truflation is a faster, and perhaps more reliable, metric.

But since onshoring of supply chains will continue to move the production of inputs as well as downstream products into more expensive jurisdictions and because the war in Ukraine does not show any signs of reaching a disinflationary denoument, inflation could remain high for much longer. If we get an economic disruption that turns on the fiscal stimulus runbook again, that would also be inflationary. Complex nonlinear phenomena like inflation tend to come in waves and misbehave in all sorts of puzzling ways. What if we get an inexplicable reflationary surge?

A fairly uncontroversial outcome of low interest rates and easy money policy in the post GFC economy has been the festival of inefficient investments in relatively unproductive assets. One possible casualty of abruptly higher interest rates could be a crash in some of those assets. If that crash materializes and turns out to be systemic in some way, how will the Fed respond? As a boringly similar example to the cause of all the trouble in 2008, take a glimpse at the Canadian housing market.

If there is no leverage involved in this situation, maybe everything is as it should be. But if there is significant leverage and we have a debt or liquidity crisis and this mean reverts, what are some of the possible knock on effects? Real estate is relatively illiquid and the rise in interest rates probably has only just started to propagate through the market. How long do we have before we find out who is swimming naked in the Canadian housing market or other inflated parts of the financial system?

Milton Friedman infamously said "Inflation is always and everywhere a monetary phenomenon." Unfortunately this frequently gets repeated in financial media circles because it gives undue credibility to the Fed's inflation response. It’s unfortunate because it implies that if inflation is always and everywhere a monetary phenomenon, then the solution must always and everywhere be monetary in nature.

Inflation is just as much a psychological phenomenon as it is a monetary phenomenon and Jerome Powell admits this in his speech from August 2020. He mentions "inflation expectations" 10 times during that speech as an important input to realized inflation. With Truflation down and with predictions of a soft landing the markets are essentially saying that we're back to business as usual despite the extremely abrupt increase in interest rates that is still making its way through the system.

Chris Irons of Quoth The Raven substack and podcast regularly describes the abruptness of the interest rate increases as a pipe bomb which is making its way through the system. While I find his vernacular delightful and the analogy compelling, I find the metaphor incomplete. The abruptness of the rate increases is more like a water hammer. When there is an abrupt change in the flow of water through a system of pipes, it can create a shockwave that propagates through the system that can cause expensive damage to plumbing fixtures. The place where the destruction happens is hard to predict and nonlinear. The damage can also happen in multiple places simultaneously. Without fixing the cause of the shock or installing buffering fixtures, simply replacing the damage is likely to result in continued problems. The debt in the global financial system is incompressible like water and the shock wave of nearly instantaneously higher rates is propagating through the international plumbing. We are already hearing pinging noises. Where will the breakage occur and who is going to get wet?

End of carry?

One disinflationary force is the massive carry trade between the USD and the rest of the world’s (ROW) currencies due to the interest rate differential. The US enjoys a discount on imports from everywhere else because the carry trade pushes the dollar up and ROW currencies down which makes ROW’s goods cheaper. In a sense, the US is exporting its inflation in exchange for real things. It’s a great deal while it lasts. But what happens when there is an inevitable crash in assets or a break in the financial system? If the Fed responds by lowering rates, this dynamic could reverse abruptly, dropping USD versus ROW, and reverse the flow of this disinflationary dynamic. If that corresponds to an increase in oil prices, we may never see double digit USD oil prices again.

The Fed is truly between Scylla and Charibdis. They are currently benefiting from some of the natural causes of disinflation such as the wearing off of fiscal stimulus and the slow global supply chain reconfiguration but since the structural causes are still present, they will likely be forced to continue to press the issue on their current policy trajectory. They have less control of the situation than market observers give them credit for but relenting on policy before there is a big problem in markets would damage their credibility.

When the proverbial makes contact with the rotating oscillator what will their response be and what will be the downstream consequences of that response? Taking them seriously about FAIT could give some clues about how long they will continue on their current path before relenting and if they persist, things could get pretty interesting. Contrary to market expectations, I think they are unlikely to pause at their next meeting. Unless there is a crash in markets between now and then, raising another 25 basis points both maintains the credibility of their seriousness and starts to slow the momentum of average inflation to keep it from substantially overshooting 2%.

That graph from Canada is staggering.